Will the West's oil price cap on Russia increase the price of

oil?

USA is now a nett

crude oil importer

Russia's view of a

buyer 'price cap' imposed on Russian commodities

Russia's

Retaliatory Ban

Who holds the

Joker?

In early September 2022 the G7 countries - Japan, USA, Italy,

France, Germany, Canada, and UK (oil buyers) - plus the EU member

countries, plus Australia, agreed they would 'cap' oil prices,

and that any 'friendly country' buying oil from Russia would have to

provide documentary evidence to shipping insurance companies that

the price they paid to Russia for the oil was lower than the cap.

This 'cap' is due to start on December

05, 2022. The 'cap' will be set slightly higher than the

Russian 'tax paid, all costs, break-even cost', which is around $20

to $44

a barrel depending on assumptions used. As at 29 November 2022 the

actual figure is still being discussed by the EU, but the most

quoted numbers are around $60 to $70, while the most rabid EU

members were holding out for $30 or so. [update: final

decision made]

""Moscow is working on mechanisms to ban the application of the

price ceiling for Russian oil, regardless of the established

level"

Russia Deputy Prime Minister Novak

We await Russia's response. I suspect it will be more than adequate.

Yet another hole will appear in the West's foot.

Whatever the final price cap, the ability to enforce it is key.

Enforcement will be through control of tanker insurance.

Importantly, a UK - based insurance association (International

Group of Protection & Indemnity Clubs) dominates global shipping

insurance - in fact 95% of global shipping is covered by association

members (most of whom are Anglo Saxons).

In principle, Russian oil could be bought by independent countries

(such as India) that refuse to impose West's 'sanctions'. But as oil

can't reach India by pipeline, it has to be shipped. Oil tankers

won't operate without insurance against oil spills, accidents,

piracy, and so forth. As almost all ship owners and charterers use

the IGPI for insurance, and IGPI is bound to obey the new EU

'sanctions', then no insurance will be available to ships from any

nation that don't apply the West's price cap - whether party to the

West's restriction or not. Very clever. Russian oil can't be

delivered, whether to India or anywhere else.

Or can it?

Russia needs 4 things. The first thing Russia needs is

customers for its oil.

"Russia will embargo countries that support the

Washington-proposed price cap on its oil...In my opinion,

this is a complete absurdity… To those companies or countries that

will impose restrictions, we will not supply our oil and oil

products, because we are not going to work under non-market

conditions”

Deputy Prime Minister of the Russian Federation Alexander Novak 01

September 2022

The rise

of Middle East and Asia Pacific oil storage and marketing hubs

Russia won't supply oil to anyone trying to apply a price cap.

That means that on, or sometime after, February 1 2023, Russia

will not supply oil (or diesel) directly to Australia, or to Europe,

Russia will not supply oil (or diesel) to USA, and Russia will not

supply oil (or diesel) to the UK. Russia will not supply oil (or

diesel) to Japan, Canada. Italy or France.

That 'only' leaves the greater part of the world's population as

customers. Russia's oil exports to China have increased. India is a

massive new market for Russian oil - in fact it now takes 40% of

Russia's key 'Urals' oil. In addition to its domestic market, India

probably 'washes' discounted Russian oil and oil products through

it's refineries by blending oil products such as Russian origin

diesel with diesel from other countries until the blend is 49%

Russian and 51% anything else. It is then regarded as 'non-Russian

diesel' and is on-sold to Europe and other markets at open market

prices.

Malaysia produces 400,000 barrels of oil a day, yet it exports

around 1.5 million barrels of crude a day to China. A large part of

the crude is obviously Russian and other crudes bought at a discount

price and then on-shipped. For example the Feoso Group (Hong Kong)

has joint ventures in China, Singapore - and Malaysia. It has a

number of oil storage sites, and it's Johor Bahru site

in Malaysia a tank farm with total storage capacity of 231,000 cubic

metres. This translates to 1,452,990 barrels of oil.Which begs the

question. Does Russian oil really unload the equivalent of 1.5

million barrels a day as various Malaysian (and other) tanks farms?

Or does it simply on-ship it direct to China.

Possibly the answer is in the stocks and flows of oil tankers of

various sizes. These complexities require a great deal of planning

and coordination, and once in place, a trading system such as this

is unlikely to be changed on a whim. Malaysia's state owned Petronas

has a vast refinery, petrochemical and product storage facility (Pengerang) in

Johor. It is a sheltered deepwater facility built to be an oil and

gas hub between the Middle East and China. As an oil importer, it

will be very pleased to receive discount oil from Russia. Perhaps it

has signed a long term contract - Petronas has already signed a 20

year contract with USA for natural gas, so long term contracts for

Russian oil would fully fit in with their 'strategic oil and gas

hub' strategy.

In any event, oil demand is picking up post covid. The Middle East,

and particularly the UAE, is becoming a storage and market hub for

Russian oil and oil products bound for Asia. Russian oil traders are

leaving Switzerland and relocating there. Russia may end up with a

slightly smaller market, but it will be enough. It is clear the

Western world (at least) is heading for a recession, perhaps even a

depression, as so much credit has been emitted to cope with covid,

and to pay USA for weapons to send to Ukraine.

The 'friendly' countries are happy to receive discounted Russian oil

(and fertiliser) as this helps reduce the effect of inflation in

these often unstable economies. In contrast, years of neglect have

meant the cost structure for energy (including decommissioning

obsolete nuclear plants) in the 'developed' West has gone through

the roof as the West, in it's radiant brilliance, has simply refused

to accept cheaper Russian gas. Soon, they will refuse to accept

'seaborne' Russian oil and oil products.

The western 'brains trust' has also refused to buy Russian and

Belarusan fertiliser. The US instigated proxy war on Russian has

resulted in disruption to feed meals for European cattle and chicken

raising industries. Once again, European prices for fertiliser and

food go up due to their European politician's maliciousness and

stupidity, while the USA is more or less self sufficient in these

areas and therefore less affected. The undeveloped countries are

also impacted by fertiliser costs and shortages, but it is becoming

clear that Russia will preferentially supply these countries.

Taken together, these factors create an unassailable argument for a

committed core of non-Western countries to turn first to Russia for

oil and fertiliser. This is called 'customer loyalty', as the

Europeans will belatedly learn. Russia has turned it's back on the

West.

"Why should Russia maintain oil production of 10 million

bpd if we can (more) effectively consume and export 7 million-8

million bpd without losses to the state budget, domestic

consumption? Which is better - to sell 10 barrels of crude for $50

or 7, but for $80?"

Leonid Fedun, Vice President Lukoil 30

May 2022

The second thing Russia needs is a profitable market. For

various reasons, oil is already in tight supply. Diesel, essential

to truck transport, is even tighter. The European portion of the

OECD countries import about 1.5 million barrels a day of oil

products from Russia - most of which is diesel and diesel precursor.

For the moment, oil products are not restricted - because the west,

and especially USA, needs it. That changes in the EU on February 5

2023, when the EU bans seaborne oil products from Russia (albeit the

EU's 'transition period' allows imports until April 2023). Russia

has already said it will stop supplying oil products to countries

that place a cap on the market price of crude oil. There will be no

lack of alternative markets.

Demand in the Asian market is growing. For a variety of reasons,

global oil refineries barely keep up with the demand for 'middle

distillates' - diesel, jet fuel, fuel oil. The price of these

products is going up and up as rate-limited throughput creates

bottlenecks in supply.

The 1.5 million barrels a day that will be diverted from Western

markets will be snapped up elsewhere at a very good price (for

Russia). In April 2023 India bought 70% of Russia's Urals oil. This

massive shift to the vast Indian market is likely to be permanent.

Russia needs relatively high priced oil to make up for any reduction

in it's market size. If the market is tight, Russia can sell a

smaller quantity of oil at a higher price - and make as much money

as they did before the West's 'price cap'.

The third thing Russia needs is ships

to carry the oil. As at August 2022 Russian-owned oil tankers are

said to carry 19% of Russia's oil exports, and Chinese tankers carry

about 6%. Greek-owned tankers carry most of the rest. Tankers flying

'flags of convenience', such as Liberian tankers, can be chartered.

Russia may simply buy

tankers to meet its (reduced) export needs.

“If you look at how many

ships have been sold over the past six months to undisclosed

buyers, it’s very clear that a fleet is being built up in order

to transport this...”

Christian Ingerslev, CEO Maersk Tankers A/S 24

October 2022

Russian tanker fleet is mostly owned by Sovcomflot, a state owned

entity. In June 2022, almost 80%

of the SCF fleet was at anchor, due to lack of insurance and

other difficulties. Some ships were put up for sale. I can guess -

and it is only a guess - that there has been a dramatic revision of

the strategic business in the ensuing months, with new structures,

new investors, new insurance.

An

oil cap would alter the flow of about

55 million barrels a month, much more if landlocked

Kazakhstani oil exported through Russian Black Sea terminals are

included (84 million barrels per month).

Russia's Unipec alone has chartered more than 10 tankers to carry

additional Russian oil to China 'the long way around'. Currently the

smaller Aframax tankers predominate, as distances were shorter. But

now larger more and larger tankers will be needed to cover the

longer distances to India and to China. Industry

analysts estimate the additional volumes will require 30

Aframax tankers, 50 Suezmaxes and over 40 'very large crude

carriers' (VLCCs). Russian Urals crude is exported mainly through

the big Baltic Sea oil exporting ports (Ust-Luga and Primorsk), and

these ports cannot accommodate VLCCs anyway - typically Suexmaxes

are the largest ships they can handle. (Some Urals crude is

also shipped through the Black Sea from the port of Novorossisyk).

Larger cargoes on VLCCs bound for the long haul to Asia are filled

via ship to ship transfer offshore Europe (offshore

Demark or Italy), usually small Aframax to a VLCC. The VLCCs

then sail via the Mediterranean and Suez canal to Asia, with most

with a final destination in India. A smaller number sail for China

(and perhaps Malaysia), but China all but monopolises Russian oil

exports from Russia's Pacific coast.

There is an existing so-called 'shadow fleet' of oil tankers, many

of them VLCC class, carrying Iranian and Venezuelan oil outside the

Western controlled shipping insurance and port handling system.

These tankers are ideal for long journeys and deep water ports in

the Asia Pacific region, and also the Middle East. This fleet is now

expanding to include smaller tankers that can access Russia's Baltic

ports.

"...while Europe happily purchases "banned" Russian oil

and gas resold from India and China (at a huge markup), its

actions have served as a gold mine for a creaky - literally -

subsector of shipping, and as Western shipping and maritime

services firms now steer clear of Russian oil to avoid falling

foul of sanctions or harming their reputations, new

companies have leapt into the void, and they're snapping up old

tankers that might normally be scrapped.

As Reuters

reports, ageing tankers have been sold in recent months by

Greek and Norwegian owners for record prices to

pop-up Middle Eastern and Asian buyers taking advantage of

sky-high charter prices for vessels willing to ship Russian oil to

India and China...with new entrants keen to get a slice of the

Russian business, second-hand oil tanker prices have

surged, especially for Aframax vessels that can carry up to

600,000 barrels, the standard size used for loading crude at

Russia's Baltic ports...The price tag for 20-year-old

Aframaxes has jumped 86% from $11.8 million on Jan. 1 to $22

million now, according to valuation company

VesselsValue....

...some of the vessels involved in shipping Iranian and Venezuelan

oil were shifting to transporting Russian oil.It estimated that

the so-called shadow fleet shipping oil from those two countries

and some of them also for Russia was made up of 107 Aframaxes, 65

larger Suezmaxes and 82 VLCCs"

ZeroHedge 7

December 2022

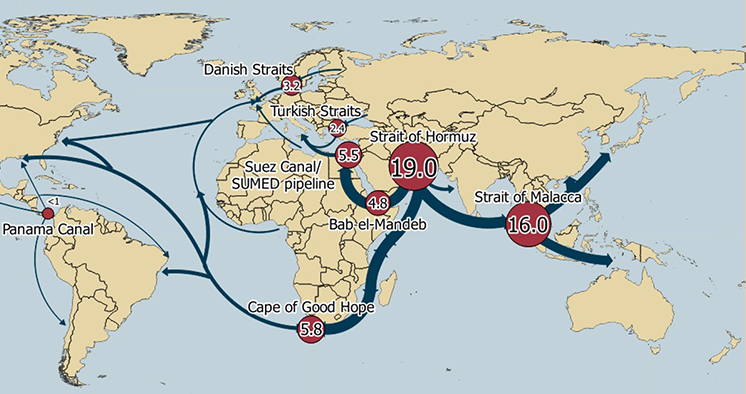

Chokepoints in seaborne oil supplies. Source:

U.S. Energy Information Administration (Jul 2017).

It is not usually economic for China to import Russian crude in

an Aframax as the lower capacity pushes up the per-barrel cost,

but with Russia selling oil cheaply to 'friendly' countries such

as China and India, the economics changes. Aframax loads to Asia

are now profitable, at least while the discount margin is so

wide.

As at early 2023 China and India take around half of Russia's

crude oil exports. India has already increased it's Russian oil

imports to 900,000 b/d from 30,000 b/d in 2021, and at

concessional prices, this is likely to increase. This

re-direction of Russian oil flow means Europe will have to

import oil from much further afield, either West Africa or . The

average tanker journey from Russia to Europe is 8 days, while a

trip from Baltic fields to India is about 22 days, and from the

Black Sea to India takes even longer - about 30 days. Baltic Sea

to China is about 37 days, but via the Black Sea takes 45 days.

Extra days sailings now required - the opposite of 'green

transport' - means extra days at sea compared to before the

restrictions, and that means extra ships are required. The

residue of scarcity of anything, ships

included, is, of course, higher prices.

This does suggest there will be a period of 'juggling' around the

availability of various classes of tanker needed for the long

journeys to carry Russian crude to West Africa, India, and China.

And temporary shortages of tankers. Even with refurbished 'old'

tankers opportunistically entering the market, some new tankers may

need to be built to plug gaps. Europe will be in the same dilemma.

No matter how you look at it, the EU restrictions increase the price

of Russian oil sailing past Europe to much further markets, and

increases the price of oil shipped from far distant sources to

Europe.

Russia can cut the distance to a

limited extent by using the Arctic route to Asia. In November 2022

Russia 'pioneered' the shipment of Arctic Sea crude, using a

specially built icebreaker tanker to cover the 5,300

kilometer journey from Russia's Murmansk to the Chinese port of Rizhao (620 km north of Shanghai). The

trip is about 40 days there and back in good conditions. Russia's

largest oil terminal is being

built at Sever Bay in the far North. This will export oil

from the Vostock fields currently being developed, with an

anticipated production of 500,000 barrels a day. Once again, the

Arctic route will be used, and obviously this means further

expansion of Russia's icebreaker tanker fleet. Insurance in this

fragile environment will be stratospherically high. Once again,

this must affect the price of the oil carried.

Even the usual anonymous

US officials acknowledge

Russia will 'probably' be able to ship almost all its own oil in

its own tankers, (owned or leased), covered by its own insurance. In

addition, Russia has start building its own Aframax class

tankers, using pre-built modules imported from China and South

Korea. The first tanker was completed in April 2023, and 3 more

are on the way. As a start.

As at 2024

S&P Global estimated that Russia was using 184 of its own or

foreign flagged small medium range tankers, 46 Panamax tankers,

260 Aframax, 84 Suezmax, and 12 Very Large Crude Carriers

(VLCCs).

The EU plans to

prohibit EU 'operators' from "financing, insuring, and

servicing" any vessel "flying the flag of a third country" for a period of 3

months AFTER their oil is unloaded in an EU port. In the

extremely unlikely event it is an EU flagged vessel,

it will be punished by EU regulations. Sailing times will now be so

long that it is conceivable that some slower tankers could ignore

the restrictions and deliver oil products to Europe, 'take the 90

day hit' after unloading. A journey to a friendly country later

(plus travel time for the next load pick up and delivery) and they

would be out of the 90 day restriction and ready to deliver 'naughty

Russian oil' to Europe again.

In early 2025 the Europeans and Americans leaned on Panama to

de-register some Panamanian flagged ships used by Russia. Trump

issued further generalised threats to impose tariffs on 3rd

countries served by Panamanian flagged ships if Panama doesn't sell

the port concession to a US controlled company. Obviously, Russia

(and other countries, perhaps BRICS countries) may as well create

it's own flagging service, whether the west puts pressure on or not.

There is one problem. It won't be loaded in Russia - they won't

supply it to Europe, whether directly or indirectly through third parties. Russian

oil and oil products will be sent to China, India, Qatar, the UAE,

or Malaysia. They can be on-sold (including to Europe) but only with

contracts that do not include the price cap. By then, the tanker

charter rate will be eye watering. What will that do to European oil

prices?

The fourth thing Russia needs is

fully insured ships (whether owned by Russia or chartered). There is

no reason why Russia cannot use state entities to fully underwrite

oil tankers. After all, oil, gas, and wheat are strategic

industries, and as such, are already majority controlled by the

Russian government. State-owned Rosneft already produces 40% of

Russia's oil, and it has recently

moved into the tanker charter business. It is a natural fit to also

do insurance.

"Despite its initial concerns, government-owned

reinsurer GIC Re will help establish an INR5 billion (SG$88.7

million) insurance pool covering India’s imports from Russia.

While officially known as the fertiliser pool, it may also be

used to insure risks of oil and gas importation from Russia,

Business Standard reported. GIC Re will contribute around 40% of

the pool, while the rest will be from an assortment of Indian

insurers, including several government-owned ones."

Insurance Business Asia 22

June 2022

The UK realised it was losing insurance business, and made a

futile attempt to rescue some of the lost business. But Russia

blocked their move.

In early August 2022 the UK removed

sanctions on insurance and reinsurance of ships carrying oil

to third countries (not the the EU). The UK is the single major

ship insurer in Europe. Russia has made it illegal to insure with

'unfriendly countries' anyway, and has developed it's own

insurance businesses for it's own ships. For example, State-owned

Sovcomflot, Russia's biggest shipping company, now insures

it's own fleet itself. through 'Russian National Reinsurance

Co'. (also state owned). The Russian National Reinsurance Company

has become the main reinsurer of Russian ships.

It must be obvious to the free-trading world that they are

vulnerable to being blackmailed by the US and the UK, who together

have the power to withhold shipping insurance on any pretext they

invent.

Russia's trading partners could spread risk by investing in

re-insurance opportunities themselves. Russia has made it illegal to

insure with 'unfriendly countries' anyway. Both China and India

already provide state insurance for cargoes of oil they buy from

Iran and Russia.

India's government-owned insurance company, the General Insurance

Corporation of India, writes reinsurance for cargoes inward bound to

India. It has a fully-owned Russian

subsidiary. While the Indian company is said to have a 60

million self-funded pool that is inadequate for a major disaster

(the Exxon Valdez supertanker, which in 1987 grounded on a reef,

causing a major oil spill, cost $780 million to settle - about $1.8

billion in today's dollars). India also draws on the global

reinsurer pool - mainly Anglo Saxon - to further spread risk and to

offer insurance for high cost but low-likelihood major claims.

Whether this pool is closed to reinsurance for Indian insurers who

might chose to insure imports of Russian oil to India (or elsewhere)

remains to be seen.

As of February 2023, Russian supplies of crude to India had

increased from 1% of India's imports to 35%. The crude is mainly

shipped on Russian tankers, and insured by Russian insurers - thus

avoiding the insurance problem. Naturally, the Indian importer pays

the cost of these services, and Russia benefits by its expansion

into the shipping insurance business.

Consequences

Short term, oil product prices will tend to be volatile.

Absent a major depression destroying world demand for oil,

petrol and diesel will never be cheap again.

Food will never be cheap again.

First, Russia will stop supplying cheaper pipeline oil to

Europe (except Serbia and maybe Hungary). Europe will have to import

oil from the Middle East or West Africa - a longer route and

therefore more expensive.

Second, supply of products such as diesel will be more

volatile. For example, Russia is a major supplier of diesel to the US East coast because US oil refineries

in the east that used to produce diesel have closed down. Without

Russia, the US East coast will have to import from elsewhere, but

supply from 'elsewhere' can be uncertain. Worse, New England (in

particular) has insufficient gas pipeline to power both home heating

and electricity generation plants - and so they have to use diesel

fuel oil when wind and solar are insufficient (such as in winter).

Electricity prices then become extreme.

“The competition for non-Russian diesel barrels will be

fierce, with EU countries having to bid cargoes from the US,

Middle East and India away from their traditional buyers”

IEA November

2022

China sharply cut its exports of middle distillates such as diesel

last year, but now that the geopolitical situation on Russia's

western border reaching a stage of predictability, if not

inevitability, China has likely filled it's very large strategic oil

reserve with cheap Russian oil, and has now released large quotas of

diesel onto the world market. If this was one result of the recent

bargaining between the leaders of China and the US, then this

emphasises the unpredictable geopolitical dimension of volatility.

This is hardly a replacement for the highly reliable regular supply

of diesel from Russia.

This increased price and availability volatility for US truckers is

'volatility of choice'. The US politicians didn't have to do this to

US transport businesses. But they chose to do it anyway, to fit

their hybrid war on Russia, a war no American voted for, and a

malicious war of choice that America is doomed to lose.

"As for green energy, let me repeat that everything

needs to be prepared for this before a final transition.

Systemic measures limiting the development of traditional

energy sources have triggered this serious crisis.

There is no funding; banks do not give loans either in Europe or

the United States. Why is everything limited? Banks do not approve

loans, do not insure, do not allocate land. Transport is not

upgraded for oil and gas shipping, and this has continued for

years. Considerable underfunding in the energy sector has led

to shortages. This is what happened.

The United States is allocating oil from its strategic reserves –

well, this is good, but they will have to be replenished and the

market analysts understand this. Today, they have withdrawn oil

from strategic reserves and tomorrow they will have to buy it

again. We are hearing that they will buy when prices go down.

But they are not going down. So what? Wake up! You

will have to buy at high prices because prices have gone up again.

What do we have to do with this? These blunders in the energy

sector were made by those who have to think about it and deal with

it."

Vladimir Putin 27

October 2022

Third, looking longer term, in line with the EIA policy,

people in Europe will demand money be allocated away from conflict

with Russia and to rapid electrification of public and private

transport, they will insist on Russian gas for industry and baseload

power while also diversifying suppliers via south European

pipelines, demand highly efficient small nuclear reactors be built,

and demand massive acceleration of programs to capture excess solar

and wind power for later use.

Fourth, In the US, people will finally come to understand

that the USA

is now a nett crude oil importer.

US 'conventional' crude oil (and condensate) has about peaked. True,

there are increasing volumes of 'oil' condensing out of natural gas

fields (this form of 'oil' went from negligible

amounts in 2010 to an astonishing 22% in 2022), but these

volatile liquids are too light. When refined, they produce volatile

light products such as propane, butane, ethane etc. They don't

produce the vital and 'heavier' middle distillates, such as diesel,

jet fuel, and fuel oil. Previously, USA imported heavy crude from

Venezuela, but after failing to overthrow the legitimate government

and install their own puppet, the USA government imposed crippling

'sanctions' on Venezuela (although in early

2023 the US government licenced 3 US oil companies to import

100,000 barrels of Venezuelan heavy crude). Absent further imports

from Venezuela, USA's energy security is now highly reliant on

Canada to provide the heavy oil to mix with the light shale

condensates. That heavy Canadian oil is expensive to produce, and

expensive to rail across vast stretches of the American continent.

Liquid condensates are also expensive to produce. Expensive to

drill, expensive to store (they re-gasify at normal temperatures and

must be cold-stored), expensive to maintain production, and

expensive to cap when the well is exhausted. It is also worth noting

that a barrel of light liquids has a lower energy content than a

barrel conventional crude oil.

The 'engine' of liquid condensate production is to a great extent

natural gas production. Light liquids, while a by-product of the

natural gas production industry, are valuable. But the US has to be

able to sell the natural gas in order to keep the liquids flowing

(and the US 'oil' production statistics up). About 20% of US natural

gas is exported, about half to Mexico and Canada, the other half

shipped as LNG. The USA has largely removed cheaper Russia natural

gas from the European market, but it can't do the same to Middle

East producers (unless it blows up the LNG tankers that transport

their gas, or sabotages their undersea pipelines coming from the gas

fields to the processing plants). The US will have competition, and

if natural gas sales slow, liquids also slow, and the US will have

to import more crude - especially middle distillates.

There are increasing volumes of natural gas liquids being produced

around the world. The USA exported very small amounts of gas liquids

in 2010, but now

exports about 2.3 million barrels a day. Those countries that

produce both light liquids from natural gas wells and also

produce heavy oils that can be blended into them have a natural

advantage. Russia is one such country.

"That's partly a function of the pandemic, after

lockdowns destroyed demand and forced refiners to close some of

their least profitable plants. But the looming transition away

from fossil fuels has also dented investments in the sector.

Since 2020, US refining capacity has shrunk by more than 1

million barrels per day. Meanwhile in Europe, shipping

disruptions and worker strikes have also eaten into refinery

production."

- Bloomberg

All against a background of American oil businesses that are

unwilling to invest much in new refineries, closing older

refineries, and re-purposing other refineries so they can deal with

biofuels and plastic re-formatting. And there is no central body in

charge, these are private-capital refineries, and act in the

shareholders best interest - not the public's. Weighing on oil

company executive's decisions in the European context is that the

European Union intends to convert some natural gas handling

facilities to hydrogen gas production facilities (processed from

natural gas). The hydrogen will then be fed through fuel cells and

similar conversion technologies to transform into electricity for

baseload power when solar and wind and hydro are insufficient. All

to help support the move to electric cars. What oil company

executive would commit large amounts of capital in an oil refinery

when petrol and diesel production seem to have a limited

future?

Fifth, the EU and USA, if they persist with this 'price cap'

plan, will, in effect, remove Russian pipeline capacity as well as

actual crude oil and oil products from Europe. As a result, other

European pipelines will become chokepoints for supply in sufficient

volumes, as will lack of European port oil terminal unloading and

tanker farm capacity.

Lastly, if Russia is forced by the West to rebalance it's

trade and turn to 'the rest of the world' as reliable business

partners, petrol and diesel prices in the West must increase in

price. Prices are likely to be volatile for some time, until the

West's farcical plans are finally abandoned.

I am confident that the EU and US will come up with some convoluted

face-saving scheme to abandon their foolish plan, but however it is

sold, the West's oil price cap will be shelved.

Russia's view

of a 'price cap' imposed by some countries on Russian oil

"Look, they are trying to put a price cap

on energy resources, on oil and gas. Who produces

them? Russia, Arab countries, Latin America, Asia, Indonesia,

Qatar, Saudi Arabia, the UAE produce oil, too.

The United States produces both oil and gas, but they

consume everything: they have little left

for the external market. That is, it is produced

in those countries, but consumed in Europe

and in the United States.

I believe

that what they are trying to do now is a remnant

of colonialism. They are used to robbing other

countries. Indeed, to a large extent, the rise

of European countries’ economies is based on slave

trade and robbery of Africa, Asia, and Latin

America. To a large extent, the prosperity

of the United States grew out of the slave

trade and the use of slave labour, and then,

of course, as a result of the First

and Second World Wars, which is obvious. But they are used

to robbing others. And an attempt

at non-market regulation in the sphere

of the economy is the same colonial robbery, or,

in any case, an attempt at colonial robbery."

- Vladimir Putin 22

December 2022

Playing the joker

The joker is OPEC+ policy. OPEC+ may decide that no OPEC+ member may

sell oil to any country that interferes with market pricing by

imposing buyer price caps.

"...just balance the books, they want to ensure a steady

stream of surpluses,” said Robert Mogielnicki, a senior scholar at

the Arab Gulf States Institute in Washington, adding that the

kingdom “would like to see prices moving closer to the high $90s.”

Saudi Arabia has the lowest oil extraction cost in the world, at

around $3 per barrel. That means the vast majority of the revenue

earned from each barrel goes into its coffers. And those funds are

needed to finance everything from futuristic trillion-dollar

cities in the desert to a sizeable government wage bill, despite

the introduction of new taxes in recent years and attempts to

diversify the economy.

“The high price [needed to balance the budget] is because of the

large spending on government services, infrastructure investment,

public sector, etc,” said Omar Al-Ubaydli...conventional tax

instruments are largely absent, especially personal income tax.”

CNN 7

October 2022

In 2019 Saudi Arabia needed an oil price of around $80 to $85 to

balance it's budget. That has changed slightly - 2022 saw Saudi

Arabia with a budget surplus for the first

time in 8 years - but Saudi budget-balancing oil target

price is is now $79.

But that does no more than balance the books. Saudi needs a good

surplus to invest further in non-oil commercial activities. Anything

that might act to suppress the price of oil is antithetical to their

interests. A severe economic recession depresses demand for oil,

reducing the price - and price-capped Russian oil would push it down

further.

By March 2025 oil prices were dropping. Spot Brent crude were at

about $74 by late March 2025, down from around $81 a barrel in 2024.

OPEC+ had a production cap in place since 2022, but planned to

remove the cap in April

2025. The Saudis have spare capacity of 3 million barrels a

day, and some of this can be brought to market very quickly if

market conditions are right. But Saudi Arabia - and some other Mid

East oil producers - are running a deficit, so price must balance

between maximising profit and not killing the market in a slowing

global economy.

The price of oil now depends on the health of the global economy.

Perhaps there will be two economies, an east and a west. One

thriving on discounted Russian oil, the other forced by Saudi Arabia

and OPEC+ to pay a much higher oil price on the open (non-contract)

spot market.

Latest

updates - most recent on top

Oil Price Cap Update 27 December 2022 : Russia's retaliatory ban

The Russian President signed the 'Executive order on special

economic fuel-and-energy measures in response to the price cap on

Russian oil and oil products established by some foreign states'.

The main part of the text is reproduced below from the official

Russian English-language website:

"Executive order on special economic fuel-and-energy measures in

response to the price cap on Russian oil and oil products

established by some foreign states

December 27, 2022

19:05

This Executive Order was signed in response to the unfriendly

actions taken by the United States, other foreign states and

international organisations that sided with them, to establish a

price cap on Russian oil and oil products, which is in violation

of international law.

The Executive Order is aimed at protecting the national interests

of the Russian Federation and is in compliance with the following

federal laws: No. 281-FZ On Special Economic Measures and Coercive

Measures of December 30, 2006, No. 390 FZ On Security of December

28, 2010, and No. 127-FZ On Measures Impacting (Counteracting) the

Hostile Actions of the United States of America and Other Foreign

States, dated June 4, 2018.

The Executive Order has established that in connection with the

ban imposed by the United States, and other foreign countries that

sided with them, on the transport of Russian oil and oil products

and related services, which is applied if the price of Russian oil

and oil products is above the limit established by said foreign

states (price limit mechanism), Russia

bans the sale of oil and oil products to foreign companies and

individuals if the contracts on these sales include the use of

this mechanism directly or indirectly.

The established ban applies to all stages of sales up to and

including the final buyer.

The ban on Russian oil sales established by the current Executive

Order becomes valid on the day of its entry into force.

The ban on sales of Russian oil products, as established by the

current Executive Order, is to be applied on the date

determined by the Government of the Russian Federation but

no earlier than the date of its entry into force.

Russian oil and oil product sales, that are banned by the

Executive Order, may be carried out under a special decision of

the President of the Russian Federation.

The Government of the Russian Federation has been given related

instructions.

The Ministry of Energy of the Russian Federation was instructed to

monitor compliance with this Executive Order based on a procedure

to be determined by the Government.

The Ministry of Energy of the Russian Federation was given the

right to release official statements on the uses of the Executive

Order with approval from the Ministry of Finance.

An interdepartmental working group on issues related to

fuel-and-energy activities was charged with ensuring compliance

with the Executive Order.

This Executive Order enters into force on February 1, 2023 and

will be valid until July 1, 2023. "

27

December 2022

It's important to note that the ban only applies if the sale price

is above the limit set by the unfriendly states. At the time the

Executive Order was signed Russian oil was selling at a price less

than the price cap, and so neither the West's ban or Russia's

retaliatory ban would apply. The price of crude will probably be

higher by 1 February 2023 when the Russian ban comes into force.

There is no set date for the Russia's ban on the sale of oil

products, such as diesel, to be introduced. It is up to the Russian

Government to decide, but it can't be earlier than 1 February 2023.

This move introduces a lot of uncertainty into the market for diesel

and jet fuel (in particular). Even if Russia does nothing, this

uncertainty is bound to spike diesel prices up in the short term.

The ban also prohibits sale of oil and oil products at " all stages

of sales up to and including the final buyer". This provision

prevents countries from buying Russia oil or diesel and simply

reselling it. It would probably have to be diluted with other

countries crude or diesel to, I guess, 51%, when it is arguably no

longer a "Russian" oil procust.

Oil Price Cap Update 6 December 2022 0155 UTC

"A traffic jam of oil tankers has formed in Turkish

waters after Western powers imposed a “price cap” on Russian oil

and Ankara demanded insurers guarantee that any vessels navigating

its straits were fully insured...In light of the price cap, four

oil industry executives said Turkey had demanded new proof of

insurance....19 crude oil tankers were

awaiting passage through Turkish waters on Monday. The ships had

anchored near the Bosphorus and Dardanelles straits, which connect

Russia’s Black Sea ports to international markets... the

International Group of P&I Clubs...stated on Monday that the

Turkish request went “far beyond” the general information normally

required...Russian insurance companies provided letters of

confirmation to Turkish authorities in order to secure passage

through Turkish waters. The shippers with insurance from western

providers were the ones being held up, according to the source."

Full story at AZGeopolitics

It appears from this article that Kazakhistani oil is not affected

by the restrictions, even though it is shipped from a Russian port

(same applies to some Azerbaijani and Turkmenistani oil piped to

Russian Black Sea ports). It is quite obvious from this

delay/blockage of Kazak oil that Turkey has extracted some sort of

concession from Russia to Turkeys economic advantage.

Oil Price Cap Update 5 December 2022: The EU price cap for

Russian crude came into effect today (the oil product cap doesn't

come into effect until February 5th 2023, ? with a transition period

until April).

Oil Price Cap Update 3 December 2022: The EU Oil price

cap finalised

The EU has decided on a price cap of US$60. The cap will be reviewed

every 2 months and adjusted to remain 5% below the International

Energy Agency benchmark.

The IEA's mission statement says 'The IEA is committed to

shaping a secure and sustainable energy future for all'. Member

countries must have a program in place to reduce national oil

consumption by up to 10%. No problem... This decision will be

formally announced in a few days time. The US

plan to collapse European industry continues to play out.

Oil Price Cap Update 28 January 2023: The EU is mooting a

'price cap' of $100 on Russian oil products, at a time when diesel

is selling into the EU at around $110 to $120 a barrel. The G7 would

like it a little higher ($100

- $110). The EU has stocked up on diesel from USA and Saudi

Arabia - and Russia - ahead of the kick-off of the ban on Russian

seaborne oil products that don't comply with the EU 'price cap'. As

a result, Russia's diesel exports hit a multiyear high. According to

oilprice.com the EU ban applies to about 1 million barrels a day of

oil products (diesel, fuel oil, jet fuel etc). As the major Russian

oil product imported by the EU is diesel, this increased demand will

drive diesel prices up.

Oil Price Cap Update 04 February 2023: The EU introduced a

'price cap' of $100 on Russian 'premium' oil products, such as

diesel and jet fuel. The EU introduced a $45 price cap on Russian

low value oil products, such as naptha. The price cap comes into

effect on Sunday 5th February, and will be followed by a 55 day

'transitional period' for seaborne cargoes that were loaded before

the 5th of February and reach their 'final destination' before April

1st.

February 5th is also the date that all EU companies will be banned

from providing any form of finance or servicing to anyone

transporting petroleum products to any country that is not

interested in applying the EU's own blockading laws to their own

sovereign affairs.

Russian non-supply to those who cap prices Update 10 February

2023: Russian oil production will be cut back by 500,000

barrels a day in March 2023. According to energyIntel

export volumes of crude will probably remain the same, but supply to

Russia's domestic refineries reduced. They claim that some Russian

refineries are shutting down for seasonal maintenance anyway.

Russia's domestic refineries have largely been configured fully

supply Russia's gasoline and diesel needs, and export

about half their excess diesel production.

"As of today, we are fully selling the entire volume of

oil produced; however, as previously stated, we will not sell

oil to those who directly or indirectly adhere to

the price cap principle. In this regard, Russia will voluntarily

reduce production by 500,000 bpd. This will contribute to the

restoration of market relations..."

- Deputy Prime Minister Alexander Novak 10

Feb 2023

If Russia's rule refers to blending Russian oil products with oil

products of other nations AND is able to enforce sale of such blends

only to friendly countries, then it will probably be able to 'short'

the supply of diesel to the EU. Obviously, if sale of Russian oil

and oil products is, in effect, prohibited from sale to Europe, then

it will drive up the price of non-Russian diesel. According to

Alexander Novak Russian oil production was 9.8-9.9 million barrels a

day the last few months despite the sanctions.

Oil Price Cap Update 10 March 2023: "New York is buying an

unusually large amount of gasoline and diesel from India — a country

that has become a top outlet for sanctioned Russian oil. " Bloomberg

By January 2023 the east

coast of USA was importing 89,000 barrels per day of 'Indian'

gasoline and diesel. Normally India would provide 5% of New York

supply - in January 2023 it had increased to 40%. Bear in mind India

is, like the USA, a nett oil importer, so the crude from which these

products are refined must have originally come from an oil exporting

country.

Index

of Laurie Meadows articles on Security