Oil and the New Zealand Economy

Laurie Meadows

Current situation

The economy is the size it is due to relatively cheap

liquid transport fuels. New Zealand (like many

countries, including USA) has used up the greater part

of its free flowing, high volume oil field reserves,

but we still manage to supply about 50% of our own

needs (2013).

That won't last. The current oil fields are dropping

in production, and Maui, the mega gas field that

produced liquids as a by-product, is a fading giant.

America has added about 9 million barrels a day of

'new' oil to its domestic supply, so it doesn't have

to buy so much from overseas. This fact, coupled with

a general global deflationary environment and slide in

oil use in the Eurozone has led to a temporary

oversupply of oil, causing prices to drop to extremely

low levels (US$47 in January 2015). Ironically, this

price is so low that oil fields with high drilling and

production cost - the 'new' shale oil fields in USA -

become uneconomic (some US shale fields are uneconomic

below about 70 USD, many are OK until oil prices go

lower than about 50 USD). At USD 47 it costs more to

bring the oil out of the shale fields than the value

of the oil that is produced. Some of these fields will

be closed off until oil prices rise again.

And oil prices will rise again, but the timing and

magnitude of the rise is related to both the economic

'state of the nations' of the world and to the pace of

natural nett depletion of the major geological oil

reservoirs.

We will find more oil, but not enough

But new Zealand is attractive enough to big and small

oil companies that they continue to search for, and

find, oil. It is unlikely that there are any major

fields in New Zealand, but a continual (for now) flow

of small fields that play out relatively quickly will

do. However, the price of oil will have to rise again

before it is worth doing.

We depend on other oil-producing countries having a

surplus to export

Our dependence on other countries export oil is

increasing. Unfortunately, major oil exporting

countries have reached the limits of their productive

capacity, and at the same time their domestic demand

is increasing with uncontrolled domestic population

growth.

We compete with every other country in the world to

buy surplus oil

At some point, volumes available for export will be

lower than global demand, and at that point oil prices

might increase significantly. But we are not at that

point yet. The

'pool' of oil available to import from overseas will

slowly shrink, but this is masked by slackening demand

and increased USA shale oil production (shale

production has meant USA only has to nett import 6

million barrels of oil a day). The effect of import

limitations won't be obvious until USA shale

production falls in 3 or 4 years time (the relatively

'high volume' shale oil resource has a very limited

life) and global economic activity starts to

grow markedly again (we shouldn't assume it will).

Price effects of Higher Oil Prices

Rising oil prices preceded 9 of the 10

recessions in the 35 years after world war 2. Higher

oil prices didn't necessarily cause the

recessions, but they very likely contributed to them.

The general economic assessment is that higher oil

prices lead to 'inflation' (in the sense of price

increases, mainly due to the direct cost of transport

fuel increasing), which then triggers the Reserve Bank

Governor to act to keep 'inflation' within the target

band of between 2% and 3%. Just about the only 'lever'

the Reserve Bank has to 'pull' is to increase interest

rates. Higher interests rates both increases mortgage

rates on home loans, and increases the cost of

business borrowing. Higher mortgage repayments by you

and me means less spending, and therefore lower

business profits. Businesses cut back on expenses by

dropping staff numbers. Unemployment rises as a

consequence.

Additionally, 'inflation' is seen by money market

traders as reducing the value of the New Zealand

dollar. It then takes more NZ dollars to buy the same

amount of oil. So even if the price of oil remains

steady, it costs us even more to import.

The process slows down and eventually stops, because

the weaker New Zealand dollar makes our exports

cheaper to buy, and the buyers have to pay us in New

Zealand dollars, which in turn creates a demand for

NZD, making the NZD more valuable. Then we get 'more

oil for the dollar' than before.

However, since 1990 rising oil prices appeared, at

first, to have had less recessionary effect.

Internationally, crude oil was still available from

2012 to mid 2014 at from $USD 80 to around USD $100 a

barrel. But we should note that from 2011 to 2013 oil

prices averaged USD110, and growth in western

economies has been constrained.

Oil prices in mid 2014 started to slide, eventually

hitting around USD 47 a barrel. It seems developed

countries have now entered a period that shifts

between low growth, slow grow, and no growth. The

result is fewer road miles traveled, particularly in

USA.

The counterfactual would suggest low oil prices would

stimulate growth in world economies.And, all else

equal, this tends to be true over the middle and

longer run. But in the immediate term, it isn't true,

because low oil prices are an effect of slowing

demand. However new car numbers (netted out from those

scrapped) have risen rapidly in 2014, particularly in

China. This insensitivity to fuel price may indicate a

growing middle class, particularly in China, or,

worryingly, it may indicate a willingness to take on

new debt by the growing middle class. New debt backed

by inflating house values.

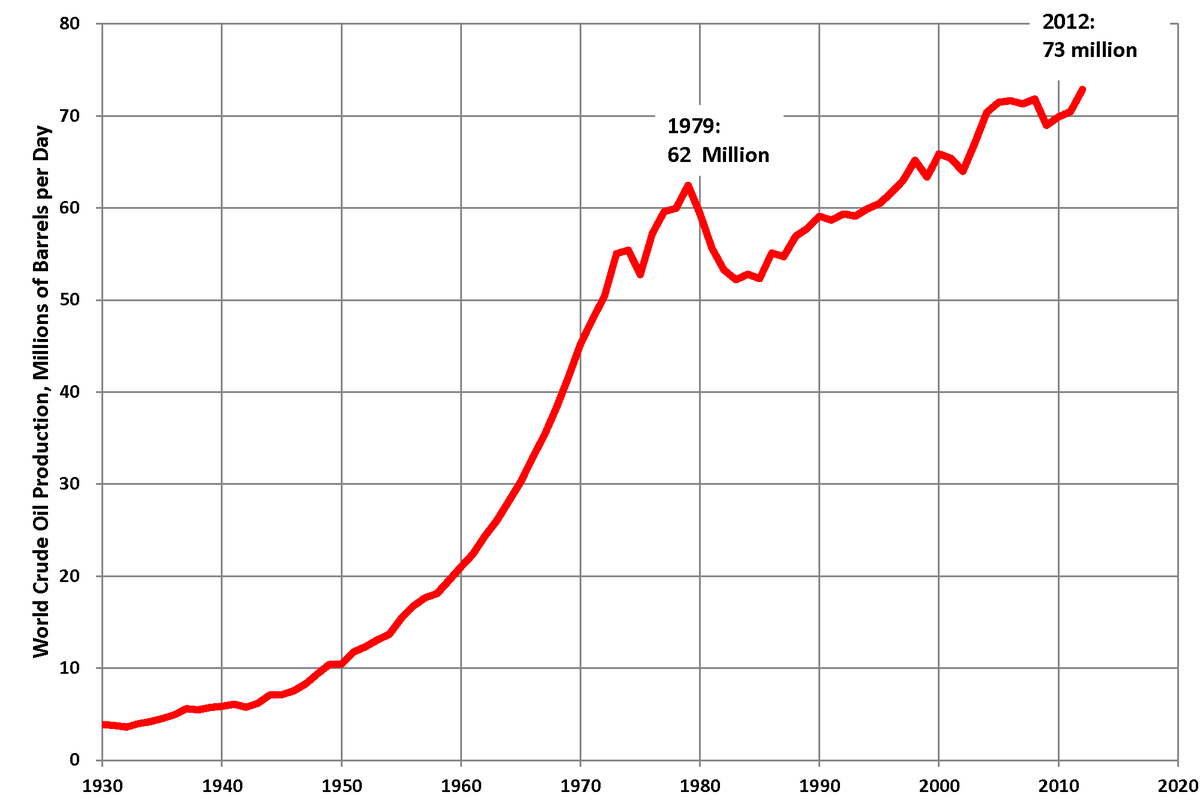

World crude oil

production 1930 to 2012

Graph: created by Plazac,

Wikipedia, reproduction licenced under Creative

Commons Attribution-Share Alike 3.0 Unported license.

Data: US Bureau of Mines and Minerals yearbooks to

1960,OPEC website from 1960, EIA 1980 to 2013

Oil supply overall is more or less static

or rising slightly

Current (feb 2015) production of around 93 million

barrels a day (mbd) takes in cheap Saudi at $25 a

barrel, to expensive Canadian oil sands only

profitable at over $80 a barrel, and everything in

between. Total global production of 'conventional'

crude oil (flowing up from an underground reservoir)

plus liquids often found in natural gas wells

('condensate') is about 77 mbd (early 2015).

Saudi Arabia, the world's largest exporter (6.9

million barrels a day of exports at end 2014, ), is

producing oil at about maximum of 9.2 million barrels

a day (down

from 9.6 mbd in 2005).

As far as limited public data can inform, it might

remain producing at these levels for a relatively long

time.

Russia

is the world's second largest crude oil exporter, at

about 5 million barrels a day of crude; but it also

exports 2 million barrels a day of refined products.

Russia's main oil supply is from heavily re-worked old

fields (at the rate of 5,000 to 6,000 'infill' wells a

year), and these are estimated to slowly decline in

production from 2016 onward. There are very large

areas of complex shale 'plays' in Siberia, but these

will take decades to delineate and fully come on line.

If oil prices remain low they will never come on line.

The rest of the world has slowly declining production

(except USA - shale oil hit 9 mbd in 2014 - but it

won't last, as the EIA says the overall production

decline rate is ~ 6.4% per month). Crude oil (45 and

lower API, excludes heavy oil) production from the

rest of the world will continue to decline at

about 7% a year over the next few years.

The pace of decline markedly increases at some point

over the next decade or so. The speed of decline at

that point depends on global demand, which in turn

depends on how deeply in recession the global

oil-dependent economy is.

The drawdown of the total 'tankload' of exportable

oil exceeds the refill rate

According to American oil commentator and oil

geologist Jeffrey Brown (February 2015) the nett

amount of petroleum liquids being exported by

the 33 biggest oil export countries was steady in an 8

year period from 2005 at 46 million barrels a day, but

exports fell to 43 million barrels a day in 2013. The

3 million barrel a day shortfall was made up by a

reduction in USA oil imports as its Shale oil industry

increased production markedly.

Jeffrey Brown notes that the 'OPEC 12', representing

the major chunk of exporters (except Russia, which

exports roughly 5 million barrels a day), exported

about 70 Giga Barrels (GB) of oil in the period 2006

to 2012. His best estimate of the portion of Saudi oil

reserves that have in the past been exported, and on

reasonable assumptions will be exported in future,

total 260 GB. This means about 27% of the total 'pool'

of exportable oil in Saudi Arabia has gone in a 6 year

period.

By about 2020, only 5 years away, the 'OPEC 12' will

have only 50% of their exportable reserves left. They

can maximise returns now by highest bearable price for

lots of customers for a shorter sustainable period, or

maximise long term returns by much cutting production

now, in the hope of not pushing the global economy

into perma-recession, and being able to levy higher

price for much longer, but for fewer customers.

Very few governments act before they have to,

especially where it means sacrifice for the population

now for a benefit later. The OPEC 12 are not likely to

be different. They are likely to 'pump full bore until

the well is dry'.

The only relevant statistic for New Zealand is oil

available for export

The press always focuses on the total amount of oil an

oil exporting country produces and any trends in that

production. The mainstream press never focuses on

trends in the percentage of oil that an oil exporting

country is using internally. While Saudi Arabia, the

world's largest oil exporter, has a growing population

and growing internal oil use, Russia, the worlds

second largest oil exporter, has a stable population,

and (I guess but don't know) internal oil use that is

pretty static.

Non OEC oil production is falling

It is widely conceded that oil production outside OPEC

is falling. Gas production globally is nett

increasing, and some gas wells have liquids associated

with the gas. These liquids are increasingly taking up

the slack in falling global conventional oil

production, just as shale oil production in the USA

has 'covered for' the underlaying decline in

conventional oil production.

In

the case of oil, supply and demand are always equal. Recession

slackens demand for oil. So recession acts as

'negabarrels' as an important factor in obscuring the

geological ceiling in 'barrels per day' oil

production.

The cost of producing oil in the Arctic, deepwater

and in Oil sand and Shale deposits is very high

It is hugely expensive to produce these kinds of oil.

This is not a problem so long as oil prices are high,

and the global economy is strong and likely to remain

strong. No unsubsidized oil company, private or

government owned, will invest big millions of dollars

in oil exploration and production if the costs of the

operation exceed the value of the oil in place. When

oil prices drop, oil development in these difficult

and extreme environment locations becomes a dead loss,

a cost. Given planning and execution of projects in

these environments takes say 5 to 10 years, investors

have to be as sure as can be that oil prices will

average high enough for long enough to cover costs, at

least.

Oil prices dropped in late 2014 early 2015, and about

1 trillion dollars worth of oil projects in such

difficult environments suddenly went on hold or were

cancelled.

New Zealand southern ocean environment is a difficult

environment. Not the worst, but still expensive to

explore and drill test wells in, let alone develop

on-ocean infrastructure for oil production. Don't

expect very much more than re-working existing fields

(unless something 'of great interest' shows up in

seismic surveys).

Politics

The largest current supply of exportable oil comes

from the Middle East, with eyes on Iraq, in

particular, to help bolster falling global

cheaper-to-produce crude oil supplies. The Iraqi's

have faced reality and admitted that their expansion

plans will have to be cut back in the face of the

political mess that is the Middle East. Saudis value

stability, but sit on a powderkeg of religious

extremism and the unmet expectations of a rapidly

growing and rapidly stratifying population. Venezuela

is clearly going to implode. Expertise in oil

production is moving away from the country.

The only bright light is that, in spite of

provocations from the West, Russia remains stable - at

least in Russian terms.

Nett outcome for New Zealand

Our dependance on imported oil will increase

inexorably, but is OK for the next maybe 4 or 5 years

(that's my guess).

Global slowdown and recession will likely hold the

price of oil oscillating at about, or a bit above,

$USD80 a barrel for the next few years.

After that it is a 3 way interplay between increasing

supply of natural gas liquids, the speed of slowing

demand due to recession, and falling absolute

availability of export oil.

Political events are a wild card on top.

Conclusion

In the worst case, fuel for our cars will remain

relatively cheap for the next 4 or 5 years due to

global recession and increasing natural gas liquids.

We won't aggressively move to electrify transport

routes and transport vehicles. Declining nett export

oil availability reaches a low enough point that it

eventually 'show through' in the form of a diminishing

pool of better-off people around the world bidding up

the price of oil.

At that point, we will realise we should have invested

in the 'future reality' years ago.

Feb 08 2015